The unfolding debt crisis in Senegal has become one of Africa’s most closely watched financial stories. What began as a routine change of government has developed into a national reckoning over concealed borrowing and the duty of governments to tell citizens the truth about the state of national finances.

For years, Senegal was regarded as one of West Africa’s more stable economies, attracting investors, development partners and lenders. Beneath the reassuring economic reports, however, lay a financial reality that would eventually raise difficult questions about openness and democratic governance. The crisis emerged after the election of President Bassirou Diomaye Faye in March 2024. Soon after taking office, Prime Minister Ousmane Sonko accused the previous administration, under former President Macky Sall, of presenting misleading financial information to international partners and lenders.

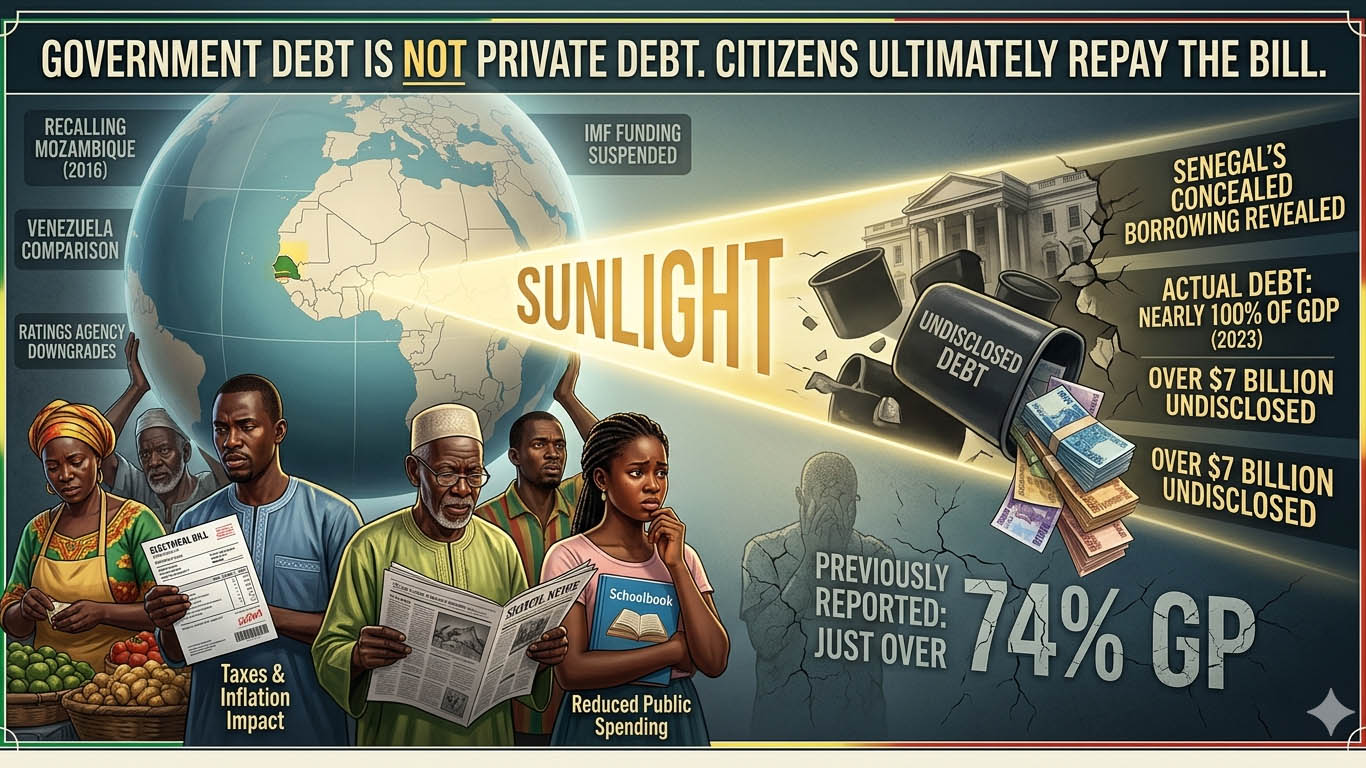

In February 2025, Senegal’s Court of Auditors confirmed that debt and budget deficit figures had been materially understated. The country’s debt at the end of 2023 was found to be nearly 100 per cent of gross domestic product (GDP), compared with the previously reported figure of just over 74 per cent. The difference represented approximately US$7 billion in previously undisclosed borrowing.

Subsequent assessments painted an even more troubling picture. Some financial institutions estimated that debt levels may have reached as high as 119 per cent of GDP once all liabilities were considered. International ratings agencies responded with credit downgrades, while the International Monetary Fund suspended discussions on new lending arrangements until the discrepancies could be addressed.

The consequences were immediate. Borrowing costs increased. Economic growth forecasts were revised downward. Government finances came under greater pressure. Most importantly, citizens were left wondering how such a large financial burden could have accumulated without their knowledge.

The figures themselves are alarming, but the broader issue is not simply the size of the debt. Many countries carry substantial debt burdens. The real concern is the apparent effort to keep portions of that debt hidden from citizens, lawmakers, lenders and development partners.

Government debt is not private debt. It is accumulated in the name of citizens and must ultimately be repaid by citizens through taxes, reduced public spending, inflation or a combination of all three. Perhaps the most widely cited example comes from Mozambique. In 2016, the country was rocked by revelations that more than US$2 billion in previously undisclosed loans had been contracted by State-owned companies with government guarantees. Donors suspended aid, the currency came under pressure and the economy entered a severe crisis. Many citizens only learnt of the liabilities after international investigations uncovered them.

Outside Africa, Venezuela provides another cautionary tale. Years of opaque financial reporting and limited disclosure made it difficult for citizens and investors to determine the true state of public finances. Economic instability followed, accompanied by declining confidence in State institutions.

These examples reveal a common pattern. Hidden liabilities may provide temporary political convenience, but they rarely remain concealed forever. Supporters of secrecy sometimes argue that governments may withhold certain financial information to preserve market confidence or avoid public panic. In rare situations involving national security, temporary confidentiality may be justified. Debt levels and fiscal obligations do not generally fall into that category. Financial secrecy often shields decision-makers rather than the public, who must ultimately carry the burden. Former United States Supreme Court Justice Louis Brandeis famously observed: “Sunlight is said to be the best of disinfectants.” Though spoken more than a century ago, the principle remains relevant today. Similarly, former United Nations Secretary General Kofi Annan once stated: “Good governance is perhaps the single most important factor in eradicating poverty and promoting development.”

Senegal now finds itself confronting precisely this challenge. The current administration has pledged reforms, improved tax compliance and greater reliance on domestic resources. At the same time, it has sought to avoid the politically sensitive option of debt restructuring. Economic growth forecasts have been reduced. Fuel subsidy costs continue to place pressure on public finances. Discussions with the IMF remain ongoing. Policymakers must now address not only financial imbalances, but also concerns regarding the credibility of State institutions.

Ultimately, the Senegal debt saga is about more than economics. It is about the relationship between governments and citizens. Should governments keep financial secrets from the people they serve? The answer should be straightforward. Citizens have a right to know the true state of public finances because they are the ones who will pay the bill. Governments may occasionally face uncomfortable truths about debt, deficits or fiscal pressures. Even when politically inconvenient, honesty remains preferable to concealment.

For years, Senegal was regarded as one of West Africa’s more stable economies, attracting investors, development partners and lenders.