News

Customary marriages declared in community of property

MBABANE – The High Court has declared the long-standing practice of treating marriages under Eswatini Law and Custom as being out of community of property unconstitutional and void. In a...

Customary marriages declared in community of property

MBABANE – The High Court has declared the long-standing practice of treating marriages under Eswatini Law and Custom as being out of community...

RESCorp sweetens diversification with E1m butchery venture

MBABANE – What began as a sugar producer has evolved into one of Eswatini’s most diversified agribusinesses. Royal Eswatini Sugar Corporation (RESCorp) has...

Mixed assets going under hammer tomorrow

MBABANE – Prospective buyers will have an opportunity to bid for a wide range of vehicles, building materials and other valuable assets tomorrow....

FINCORP, IDCE rivalry reshapes development finance landscape

MBABANE - Competition between FINCORP and IDCE has reached unprecedented levels as the two development finance institutions battle for market dominance while expanding...

Eswatini, Egypt discuss cooperation, gold bank initiative

MBABANE - The Central Bank of Eswatini and Egypt have explored closer banking cooperation, focusing on cross-border payments, financial integration, gold reserves and...

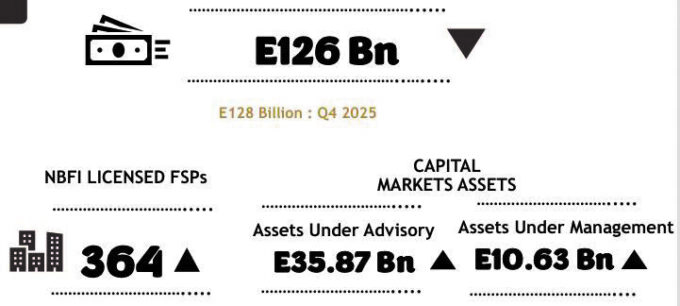

SBS conversion drives NBFI assets’ E2bn drop

MBABANE – The non-bank financial institutions (NBFI) sector has recorded a nominal E2 billion decline in total assets following the reclassification of Swaziland...

Lidwala leads short-term insurance sector

MBABANE – Lidwala Insurance has overtaken long-time market leader Eswatini Royal Insurance Corporation (ESRIC) to become the largest short-term insurer by gross written...

Civil servants’ extra 10 per cent allowance suspended

MBABANE- The additional Central Agencies Allowances of 10 per cent on top of the recently implemented 85 per cent salary adjustment has been...

25 foreign nationals nabbed attempting illegal border crossing

MHLUMENI – Twenty-five foreign nationals were arrested at Mhlumeni Border Gate on Saturday after allegedly attempting to leave Eswatini without the required travel...

LiSwati comedian wins girlfriend back in boxing ring

MBABANE- Most guys buy flowers to win back an ex, but this Eswatini comedian had to dodge a barrage of leather in the...

Chinese nationals challenge re-arrest

MBABANE - The 25 foreign nationals from the People’s Republic of China are challenging their re-arrest and detention at Mafutseni Police Station. The...

Pilot outsmarts Fokker 28 hijacker, earns King’s medal

MBABANE - Retired Eswatini Air captain Robert Dlamini still vividly remembers the night an ordinary flight turned into a life-or-death ordeal. In July...

Latest Videos

BIGGEST BRAAI 2026

27 July 2026

STORY BEHIND ESWATINI's ATHLETICS | THE FAST BREAK S1 E1

24 July 2026

HEADLINES | JULY 24

24 July 2026

How is Eswatini's Sugar Industry performing?

20 July 2026

HEADLINES | 20th JULY

20 July 2026

CABULA CHURCH | ALCOHOL DURING CHUCH SERVICE | A LOT OF CONTROVERSY

17 July 2026

HEADLINES | 17 JulY

17 July 2026

Headlines | JULY 16

16 July 2026

ERS CLIENT APPRECIATION DAY 2026

15 July 2026

Sports

Malanti put E100k price tag on Mfundo

MBABANE – He will not come cheap! Malanti Chiefs’ highly-rated star and 2026 Instacash Schools Ball Games Player of the Tournament Mfundo ‘Luuh’ Kunene has drawn immense interest from a...

Comments and Analysis

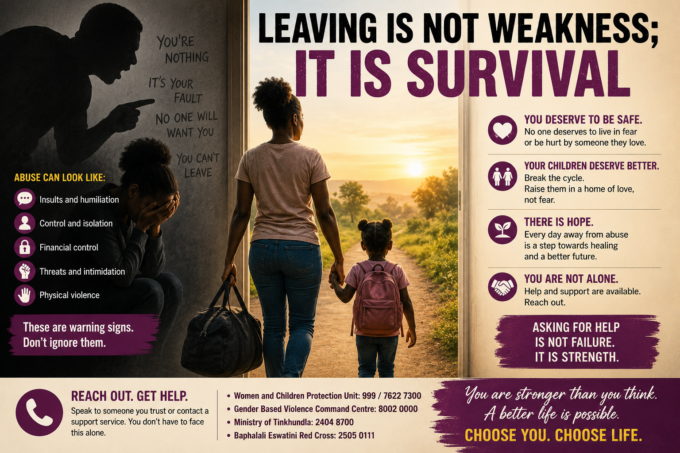

Leaving is not weakness; it is survival

There is a question people often ask after hearing about another tragedy involving a woman and her children: ‘‘Why didn’t she just leave?’’...

Faith is free, fees are not!

I grew up in church. Not the kind where your mother threatened to pray the stubbornness out of you, but the kind where Sunday...

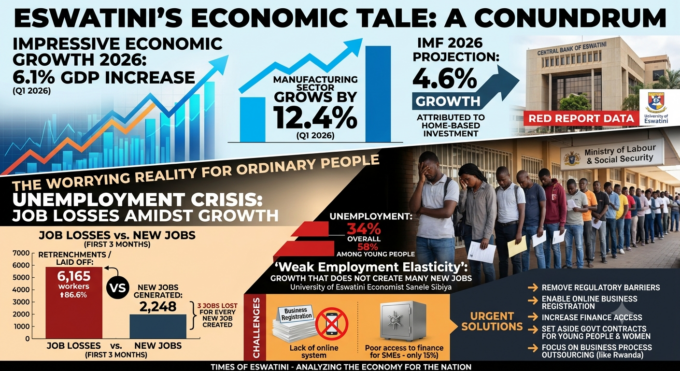

Good growth needs agile strategies

The latest economic growth figures are telling a story we are excited to hear. The economy grew by an impressive 6.1 per cent...

The calendar never loses!

I have finally settled the GOAT debate. It wasn’t Lionel Messi. It wasn’t Cristiano Ronaldo. It was a calendar. Turns out calendars are...

Training and Education

Maturity transforms learning into purpose

In today’s fast-paced, ever-evolving world, learning has become more than just a phase, it is a lifelong commitment. For individuals like Thobeka Zwakele Mkhonta, a Bachelor of Commerce student at...

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}