Our economic debate often circles around familiar challenges: Slow growth, high unemployment, dependence on volatile SACU revenues and persistent inequality. Yet quietly, a powerful opportunity is emerging, one that does not rely on extractive industries, massive capital inflows, or external transfers. Financial technology (Fintech), if deliberately aligned with inclusive financial policies, can become one of the country’s most effective growth engines.

At its core, Fintech is not about apps or algorithms; it is about access. It is about who can save, borrow, insure, invest and transact safely and affordably. In a country where many micro and small enterprises remain informal, women entrepreneurs are under-financed and young people struggle to turn ideas into livelihoods, inclusive finance can fundamentally reshape economic participation.

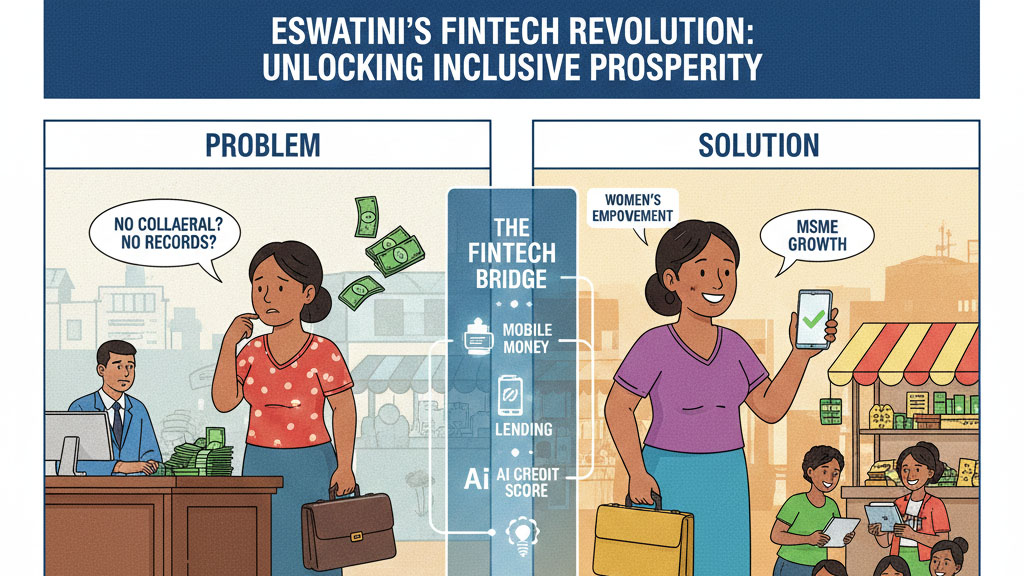

MSME’s: Survival to scale

MSMEs form the backbone of the country’s economy. They dominate retail trade, agriculture, services and the informal sector. Yet, they remain chronically constrained by limited access to finance. Traditional banking models often require collateral, formal financial records and credit histories that many small businesses simply do not have.

Fintech can change this equation. Digital payments, mobile money and alternative credit scoring systems allow financial institutions to assess risk using transaction histories, mobile usage and business cash flows, rather than land titles or fixed assets. This means a market vendor, a small farmer, or a township service provider can gradually build a digital footprint that opens the door to credit.

When small businesses can access working capital, they move beyond survival. They invest in inventory, equipment and technology. They hire labour. They formalise operations and contribute to the tax base. In this way, financial inclusion becomes not just a social intervention, but a macroeconomic intervention expanding productivity and domestic demand.

Closing the finance gender gap

Few economic reforms have as high a return as empowering women financially. In the kingdom, women are active economic agents, running small enterprises, managing household finances and driving local markets. Yet, they face systemic barriers to accessing credit, including asset ownership disparities, lower formal employment and discriminatory lending practices.

Fintech provides an opportunity to narrow this gender finance gap. Mobile banking platforms allow women to control their own accounts privately and securely. Digital savings products enable incremental saving, which aligns with the income patterns of many women entrepreneurs. Micro-insurance products reduce vulnerability to health shocks, climate risks and business disruptions.

More importantly, data-driven financial services can decouple creditworthiness from traditional biases. When loans are assessed based on business performance, rather than marital status or asset ownership, women entrepreneurs gain a fairer chance to access capital. The result is not only improved livelihoods, but stronger household welfare outcomes, including better nutrition, education and health spending.

Financial inclusion as economic participation

Financial exclusion is a form of economic exclusion. When individuals operate entirely in cash, they are invisible to the financial system and largely excluded from policy tools designed to support growth. Digital finance brings people into the formal economy, not through coercion, but through convenience and opportunity.

For young people, Fintech lowers the barriers to entrepreneurship. Digital wallets, online marketplaces and low-cost payment systems make it easier to start small ventures with minimal upfront costs. For rural communities, mobile money reduces geographic barriers to banking and improves access to remittances, government transfers, and agricultural finance.

At the national level, broader financial inclusion improves economic governance. Digital transactions enhance transparency, reduce leakage and support better targeting of social and economic programmes. They also create valuable data that policymakers can use to understand consumption patterns, enterprise growth and regional disparities.

Inclusion is not automatic

While Fintech holds promise, its benefits are not automatic. Without deliberate policy choices, digital finance can deepen inequality, excluding those without smartphones, connectivity, or digital literacy. This is why inclusive financial policies must accompany technological innovation. Firstly, regulatory frameworks should encourage innovation while protecting consumers. Clear rules around digital lending, data privacy, and cybersecurity are essential to build trust. Predatory digital credit practices, already seen in other countries, must be proactively prevented.

Secondly, digital infrastructure investment is critical. Affordable internet access, reliable mobile networks and interoperable payment systems are public goods that enable private innovation. Without them, Fintech remains an urban privilege.

Thirdly, financial literacy must be prioritised, especially for women, youth, and rural populations. Understanding digital products, interest rates and consumer rights empowers users to make informed decisions and avoid over-indebtedness.

Finally, Fintech strategies must align with national development goals. Financial inclusion should support productive sectors such as agriculture, manufacturing, and services, not merely consumption-driven lending.

Strategic opportunity

The kingdom stands at a crossroads. As fiscal pressures mount and traditional growth drivers weaken, the country must look inward to unlock the economic potential of its people. Inclusive finance offers a pathway to do just that.

By enabling small businesses to grow, empowering women entrepreneurs, and expanding economic participation, FinTech can help transform the country’s economy from one characterised by exclusion and vulnerability to one driven by opportunity and resilience. The question is no longer whether financial inclusion matters but, whether we are bold enough to make it pivotal to our development strategy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment